We trust you are well.

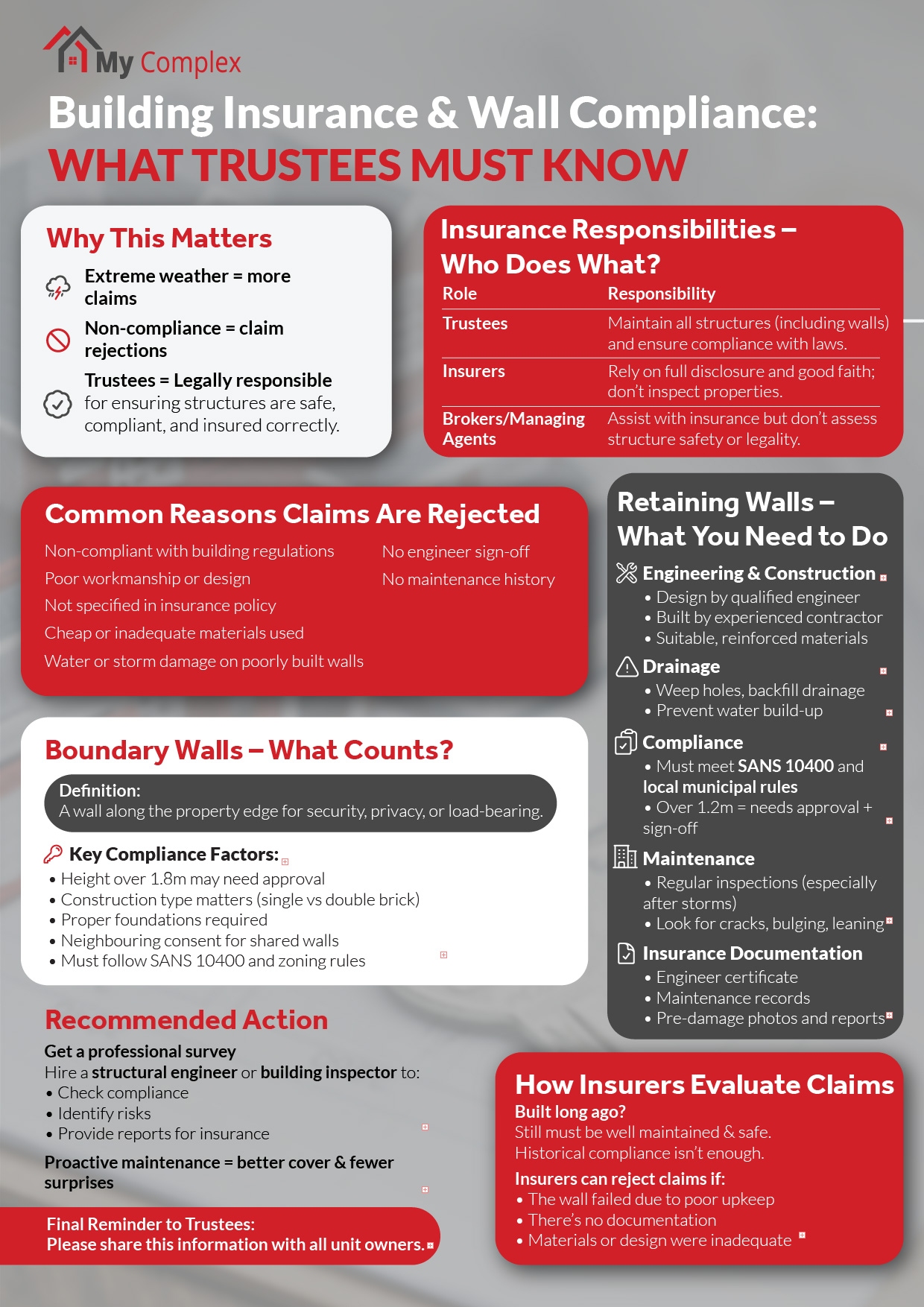

Following recent extreme weather events, we have seen a sharp rise in structural claims, especially where walls or buildings were not compliant or maintained. Unfortunately, insurers are within their rights to decline claims in such instances.

We would like to bring to your attention some important key information regarding the roles and responsibilities of all parties involved in the insurance of your building, especially in relation to structural issues such as boundary and retaining walls.

Kindly confirm that this has also been circulated to all unit owners, as it contains critical information regarding the limitations of cover, particularly relating to boundary and retaining walls and the legal responsibilities under the Sectional Titles Schemes Management Act.

Retaining walls is a general exclusion, unless insurers grant cover based on the requirements. Once cover is granted there will be an additional premium charged as per the sum insured for the retaining wall.

Key Points Regarding Building Insurance Responsibilities

- Trustee’s Responsibility Under the Law:

As per the Sectional Title Schemes Management Act, Trustees are responsible for ensuring that all structures (including retaining and boundary walls) are maintained and comply with national building regulations and municipal by-laws. - Insurers Rely on Good Faith:

Insurers do not conduct structural assessments or surveys before granting cover. Insurance is issued on the principle of utmost good faith, meaning it’s the responsibility of the property owners (via the Trustees) to disclose all material facts and ensure the building is in sound condition. - Brokers and Managing Agents Are Facilitators:

We assist with placing and maintaining the policy but are not qualified to determine the structural adequacy or regulatory compliance of the property.

Retaining and Boundary Walls – Common Claim Issues:

We have seen a large number of claims declined for the following reasons:

- Non-compliance with building regulations

- Poor or absent maintenance

- Lack of engineering oversight in construction

- Storm or water damage where the wall was not built to standard

- Retaining walls which are not specifically specified on the policy

- Ineffective construction

- Poor workmanship

- Inferior products and material used

Increase in Structural Claim Declines:

Severe weather conditions have exposed numerous structural shortcomings, particularly with retaining walls. These issues are often not covered by insurance due to the reasons mentioned above.

Recommended Preventative Action:

We strongly recommend appointing a qualified building inspector or structural engineer to conduct a compliance and maintenance survey of the complex. This proactive approach can help ensure the building is properly maintained and appropriately insured going forward.

Guidelines for Retaining Walls – Insurance & Compliance

To ensure your retaining walls are both structurally sound and insurable, please adhere to the following minimum requirements:

✅ Engineering & Construction Standards

- Must be designed by a qualified structural or civil engineer, especially if the wall exceeds 1 meter in height.

- Construction must be done by a registered contractor, with experience in retaining structures.

- Use of appropriate materials (e.g., reinforced concrete, interlocking blocks, gabions) suited to soil and slope conditions.

✅ Drainage & Water Management

- Proper drainage systems must be built into the wall (weep holes, backfill drainage) to relieve hydrostatic pressure.

- Ensure effective slope grading and redirection of surface runoff away from the wall.

✅ Municipal & Regulatory Compliance

- Must comply with South African National Building Regulations (SANS 10400).

▸ View regulations here: https://www.sans10400.org.za/ - Walls exceeding 1.2 meters typically require municipal approval and engineer sign-off (this varies by municipality).

- Building plans for retaining walls should be approved and filed with your local authority if required.

✅ Maintenance Requirements

- Walls must be regularly inspected and maintained. Signs such as cracks, bulging, leaning, or water seepage are red flags.

- Regular assessments are strongly advised, especially after severe weather.

✅ Required Documentation for Insurance Claims

- Engineering certificate, only for retaining walls

- Proof of regular maintenance or inspection

- Photos and written condition reports (especially pre-damage)

Please Note: If a retaining wall is found to be non-compliant or poorly maintained, insurers may lawfully decline any related claim. Responsibility for ensuring compliance lies with the Trustees as per the Sectional Title Schemes Management Act.

Boundary Wall – Definition and Regulatory Guidelines

Definition:

A boundary wall is a wall that is constructed along the boundary of a property, typically to demarcate property lines, provide security, privacy, or serve as a retaining or load-bearing structure in some instances. It does not form part of a building’s structural envelope but may still have implications under local planning or building control regulations depending on its height, location, and method of construction.

Typical Regulatory Considerations for Boundary Walls:

Reference; https://www.sans10400.org.za/

Building Control Officers (BCOs) should assess the following aspects:

- Height of the Wall:

- Any wall over 1.8 meters in height may require building approval depending on the municipality or local authority.

- Walls under 1.8m are often exempt from approval but may still need to comply with planning regulations (e.g. aesthetics, zoning).

- Type of Construction:

- Example: a Building which was constructed 20 years ago, the standard a 1.8-meter single-brick wall was commonly accepted as sufficient and did not typically raise structural concerns.

- Example: a building which was constructed not too long ago the standard is now, a 1.8-meter wall is now generally expected to be double-brick or have reinforced piers or supports at intervals. Some municipalities may require specific reinforcement details or damp-proofing depending on the wall’s proximity to buildings or the water table.

- Foundation Requirements:

- Even boundary walls require suitable footings, typically around 230–300mm wide and 400–600mm deep, depending on soil conditions and wall height/type.

- If located near public spaces or driveways, stricter structural requirements may apply.

- Neighbouring Consent and Party Wall Considerations:

- If the wall is being built on a shared boundary line, a party wall agreement or formal neighbour consent may be necessary, especially if the wall will affect adjacent structures or access.

What BCOs Should Look Out For:

- Confirm if the wall height and construction comply with the latest municipal or SANS (South African National Standards) requirements.

- Ensure correct wall thickness, especially for walls over 1.2 meters.

- Check for adequate support structures like piers or reinforced corners.

- Verify foundation depth and width appropriate to soil type and load.

- Confirm stormwater runoff or drainage considerations if the wall may affect water flow.

- Be alert to zoning limitations or if the wall interferes with building lines or sight lines on corner properties.

How Insurers Handle a Possible Claim:

When assessing a potential claim, insurers typically refer to the building regulations that were in place at the time the structure was originally constructed. However, it is important to note that claims can still be repudiated based on other factors, regardless of compliance with historical regulations.

These factors may include:

- Incorrect sand-to-cement ratio in the mortar

- Insufficient use of brick force or reinforcement

- Poor workmanship or materials not meeting the minimum standards

Even if the building met the regulations at the time, substandard construction practices can result in a denial of the claim. Therefore, it is essential to ensure that construction meets not only regulatory requirements but also industry best practices.

Lydia from My Complex is available to assist with referrals to independent building inspectors should you wish to proceed with a maintenance survey. Simply email her at Lydian@mycomplexsa.co.za to get connected with a qualified professional.

Please do not hesitate to contact us if you require alternative information.

Kind Regards

ASI Bestsure – Sectional Title Team